The number. How much do I need? Pt-2

In Part 1 we talked of helping you arrive at a ‘good enough’ understanding of your number for your financial flexibility. There was some prep work –

- How much do you spend today?

- In how many years do you seek to be financially flexible?

- How much do you have already in assets, after taking out liabilities and loans?

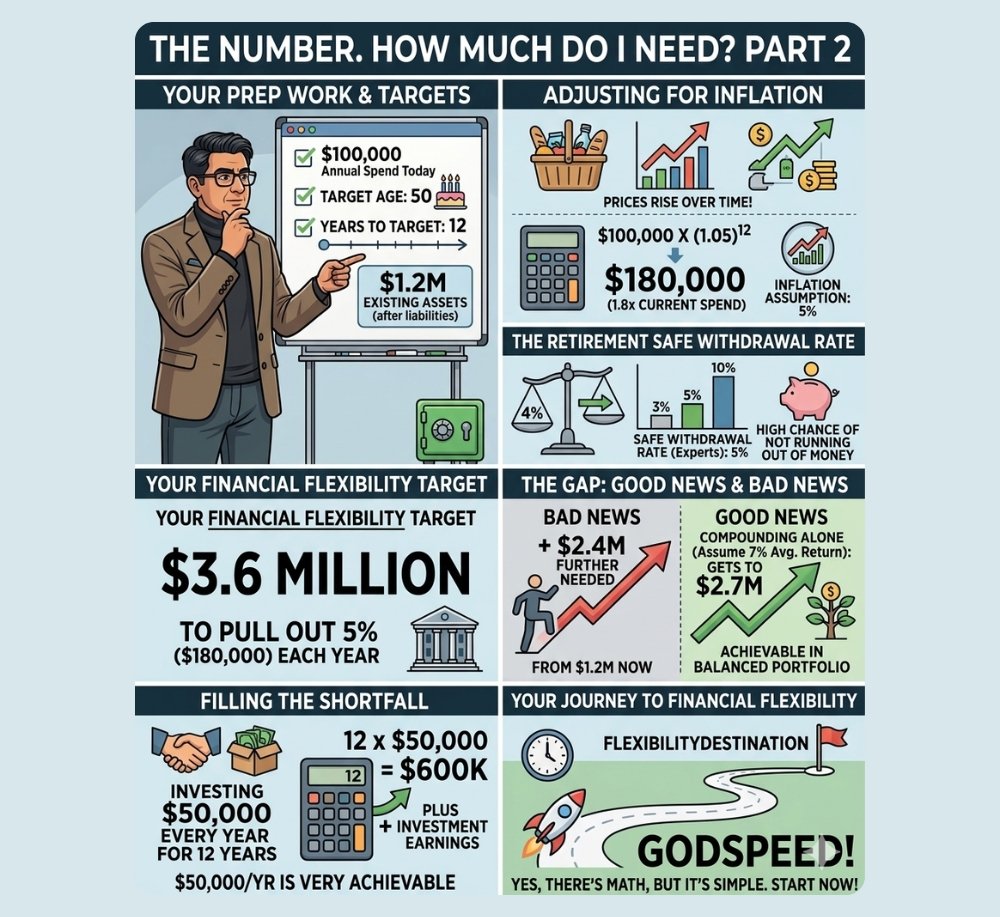

Let’s assume you figure out you spend around $100,000 each year. You are 38, and are seeking to be financially flexible by 50. My target age. That means, in 12 years from now.

The first adjustment you have to make is of inflation. Prices in the future would be higher than they are today. $100,000 wont go as far in 12 years as it does now. So you must ‘inflate’ the amount you need. Go with the higher of either the inflation you see yearly where you live, or 5%. Reason? In much of the world, annual inflation runs between 3-5%.

If using a calculator, take 100,000 and multiply by 1.05. And do this 11 more times to the answer, to get at what you need in 12 years. Or, 100000 X (1.05)^12

This gets you to $180,000 after 12 years. Or put simply, if you spend $100K now, you ill need $180K or 1.8 times your current spend to maintain a similar lifestyle after 12 years.

Now to figure out HOW to get $180K every year after you reach 50.

Various experts have established that a ‘safe withdrawal rate’ of 5% every year (adjusted each year for inflation) leaves you with a high chance of not running out of money. While many sources go as low as 3% a year, and others go as high as 12%, reminding people that markets can return around 10% every year, I find 5% a more realistic number to work with.

This means in 12 years you would need $3.6 Million to be able to pull out 5%, i.e $180,000 every year, and then increase it in step with inflation.

Now there’s the bad news and the good news.

First the bad – you will need a further $2.4 million to get from the $1.2M you have now to the $3.6M you need to get to. In just 12 years.

Now the good news. Assuming an average return of 7% a year – quite achievable in a balanced portfolio – compounding alone gets you to $2.7M, closing more than half your gap.

The shortfall? Investing just $50,000 every year over these 12 years, closes off that shortfall once you factor in the earning on that investment over that accumulation time.

While $2.4 million more over 12 years sounded almost impossible, $50,000 every year for those 12 years seems very achievable.

Yes, this has some math. But it is simple. If you literally punch the numbers into your calculator or spreadsheet, the answer is easy. And achievable, the earlier you get started.

Enjoy the journey to your financial flexibility. And Godspeed!