The ‘Sleep Well at Night’ Wealth Plan

I often get asked about how I would describe a plan that would let me sleep well at night.

Is it possible? I would say…YES. A personal financial plan isn’t a physics or a math problem. Precise inputs, with complex formulae, resulting in a super-accurate answer.

The real world is messy, and humans are even messier.

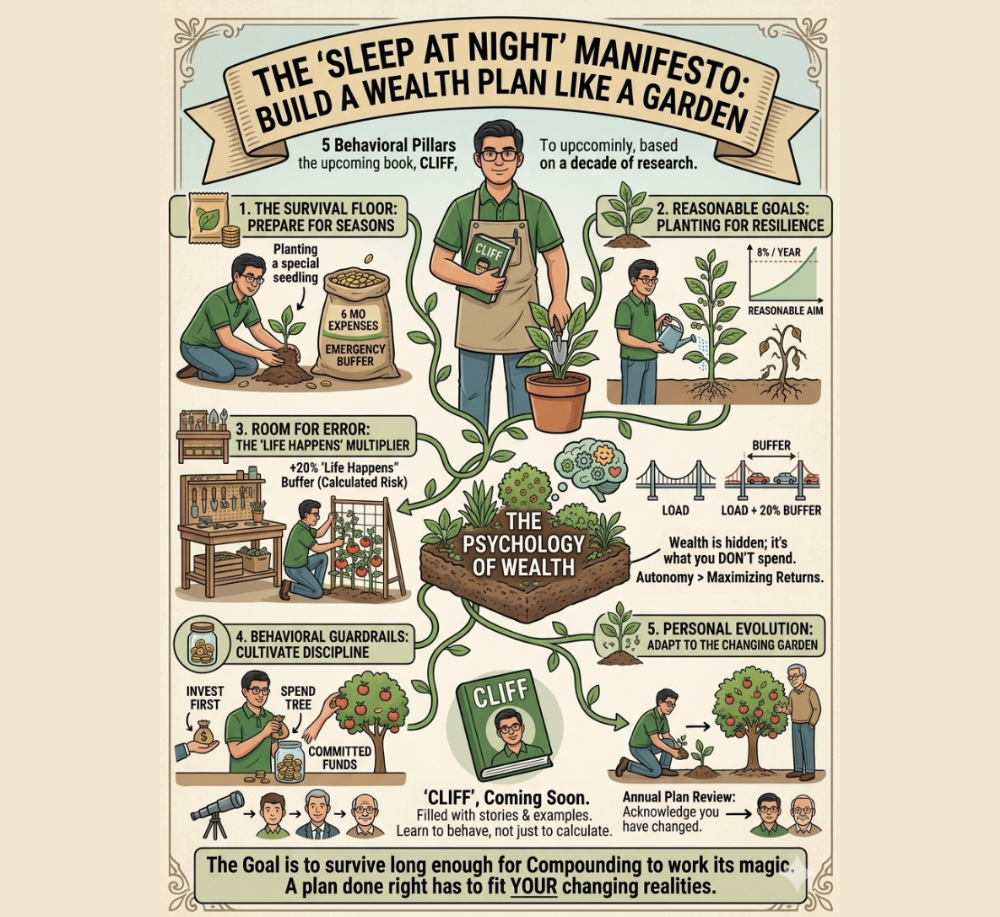

If you want a plan that lets you sleep when the markets are screaming, I find it comes down to five elements that are built into the plan. I liken it to building a personal garden.

- The Survival Floor – prepare the garden for all seasons

You can only stay invested for the long run if you can survive all seasons – the good and the bad. Some cash – your personal emergency fund – isn’t a ‘drag on returns’ – it is an insurance policy against having to make a bad financial choice.

I aim for six months of living expenses. I also strongly recommend setting up a credit line against some of your invested assets as a secondary safety net. This ensures that you never have to sell a great asset at a terrible price just to pay the electric bill.

- Reasonable vs. Rational – planting for resilience

A ‘rational’ investor wants to beat the market every year. A reasonable one, on the other hand, recognizes that resilience matters more. Over the last century, the market averaged roughly 10% annually: half the time it was below that, and half the time it was above.

My goal is to achieve financial flexibility. So I plant my financial garden for resilience by diversifying. Every dollar doesn’t go into stocks. Some go to bonds, gold, even to atypical assets. I seek to hit an 8% annualized return over a rolling three-year period. Why? It fits the inevitable bad years, and helps me be resilient to let compounding work its magic.

- The Room for Error – expecting unexpected storms

The biggest risk is the one you don’t see coming. Just as some unexpected storms are very likely, tearing up parts of the garden, life too will have gaps between what you think will happen and what happens.

Whatever your magic number is for retirement or flexibility, add 20%. I call it the ‘Life Happens’ Multiplier. This isn’t because you’re bad at math; it’s because the world is good at surprises. That buffer is for the curveballs, the calculation errors, and the ‘once-in-a-century’ floods that seem to happen every decade.

- Behavioral Guardrails – disciplined gardening

Green shoots don’t happen one day after planting. For a garden to grow you need regular and disciplined gardening. The best way to do that in a personal finance portfolio is to automate the discipline.

Regular automated monthly investing, and target date funds that annually rebalance are good examples of this. My strategy? Any unplanned expense over $100 should wait a day. This creates friction. That small barrier to spending cultivates a habit of consciousness.

- The End of History Illusion – regrow and redo

We are all walking works in progress who mistakenly think we are finished. The person you are at 25 has different dreams than the person you will be at 45. Acknowledge your own personal evolution. Your risk tolerance will shift. Your definition of ‘enough’ will change.

Your garden doesn’t HAVE TO be the way you imagined it years ago. I review my plan annually to check if it still aligns with the person I’ve become.

The ultimate purpose of a financial plan isn’t to die with the biggest pile of money. It is to ensure that you never have to stop playing the game before you’re ready. The numbers on the screen are just the scoreboard; the prize is the ability to sleep soundly, knowing that your personal financial ‘garden’ will be your relaxing, comfortable space through your life.