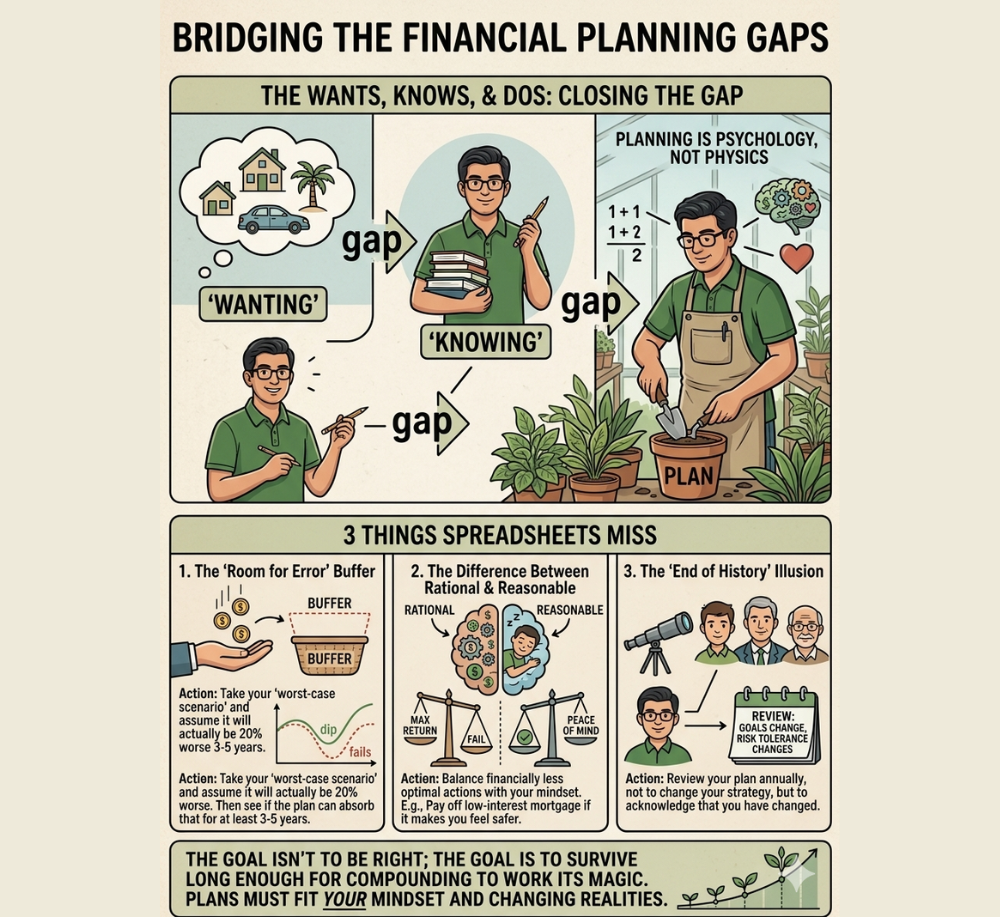

Wanting. Knowing. Doing.

When it comes to personal financial planning, there is often a big gap between ‘wanting’ and ‘knowing.’ And an even bigger gap between ‘knowing’ and ‘DOING.’

This is because financial planning is often treated like a physics problem rather than a psychology issue.

The math of wealth is simple. The behaviour is incredibly hard.

To get from understanding to an actual plan that works, look for 3 things that spreadsheets miss:

- The ‘Room for Error’ Buffer

Life rarely goes perfectly as imagined. A good plan calculates how much of a beating your ego and bank account can take before you give up.

Action: Take your ‘worst-case scenario’ and assume it will actually be 20% worse. Then see if the plan can absorb that for at least 3-5 years.

- The Difference Between Rational and Reasonable

A rational person tries to stretch every dollar, while a reasonable person realizes they need to sleep at night. If paying off your low-interest mortgage makes you feel safer than investing that cash, do it. The best plan is the one you can stick with for 30 years.

Action: Balance financially less optimal actions with your mindset

- The ‘End of History’ Illusion

We are all under the delusion that the person we are today is the person we will be in ten years. Over time goals change. Risk tolerance changes.

Action: Review your plan annually, not to change your strategy, but to acknowledge that you have changed.

The goal isn’t to be right; the goal is to survive long enough for compounding to work its magic. Plans done right have to fit with YOUR mindset and your changing realities.